“Naked” options writing brings substantial profit potential, but also high risk. Here are ten ways to help mitigate that risk and reap greater rewards when executing this type of strategy.

When it comes to options trading, it doesn't get much sexier than playing it naked. No, I'm not referring to what you wear (or don't) when you're sitting in front of your computer trading (that's your business alone). I'm talking about naked options writing.

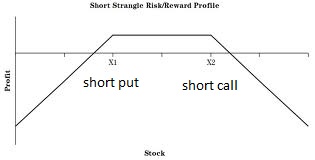

While covered options writing ("covering" your option writing risk by owning the underlying stock) is a conservative strategy that offers only part of the benefit of options writing, naked options writing (selling options without the stock covering your position) allows you to reap all of the benefits and profit potential option writing has to offer. It doesn't get much sexier than that, people!

While the potential rewards from writing naked options are outstanding, and the odds of winning are strongly in your favor, there are some substantial risks. In fact, there is unlimited risk when writing naked calls, and extensive risk when writing naked puts—the risk that the underlying stock will move through and far above or below the options strike price.

This highly publicized risk scares many investors away from this strategy, and many naked options writers have lost their shirts (pardon the pun). But although the risk is real, it is usually greatly exaggerated, and if you follow the guidelines I'm about to share with you, you will control that risk and reap the rewards that this game offers.

Set a Bailout Point and Use It

A bailout point is the price, or the point in your strategy, at which you wish to buy back your naked positions in order to limit your losses. This is the point at which you will bite the bullet if things don't go your way, and it is the most important component of your naked option writing strategy. You must use this as a safeguard to limit your losses and control the tremendous risks involved with this strategy.

As an options writer, you have the right to go into the market at any time and buy back your naked options, thereby limiting all possible future losses. Setting a bailout point is a way of insuring that you will use this right when the price hits the parameters you have set.

I strongly recommend using a stop-loss order rather than a mental stop. And it is better to set your stop loss based on the underlying stock's price, as opposed to the option's price, because options prices are more erratic, and in many cases, they may become extremely inflated even though the stock price has not moved accordingly.

Write Naked Calls in Bear Markets; Naked Puts in Bull Markets

This secret of naked option writing is self-explanatory. To improve your probability of winning in this game, it is far wiser to write calls when stock prices in general are moving down and write puts when stock prices are moving up.

This strategy will put the odds in your favor. However, writing naked call options in bull markets can be profitable, as can writing naked puts in bear markets, because of the inherent advantage the naked option writer holds. By following these rules, you will improve your probability of winning the game and reduce some of the risk.

Don't Buck the Trend

Your profits will be much greater in the naked option writing game if you write calls when the underlying stock is moving downward and write puts when the underlying stock is in an uptrend.

The best way to project this type of price behavior is to look at the underlying trend of each of the optionable stocks. Never buck a strong uptrending stock, or in Wall Street parlance, "Don't fight the tape."

Select Stocks with Low Price Volatility

While the option buyer always hunts and pecks for options on stocks that are extremely volatile, the option writer loves stocks that don't move anywhere. He wants stocks that move slowly, and ones that move in a narrow range, because the option writer always has time working in his favor.

The slower a stock price moves, the more money he makes. Options with slow-moving underlying stocks will depreciate to zero before the stock ever reaches the bailout point.

Unfortunately, the stocks with the highest volatility maintain the highest and fattest premiums for option writing, and so the option writer must attempt to find options with low volatility, and correspondingly high premiums (time values) when possible.

Diversify

Naked option writing, with its extreme risks, requires diversity. You should maintain at least four different option positions with different underlying stocks.

Remember, one of your overall goals is to stay in the game, and the best way to do that is to avoid betting all your money on one horse. Although the odds are heavily in your favor, losers can put you out of the game if everything you have is bet on that one position.

Finally, maintain very small positions in each stock so that a takeover does not nail you with a devastating loss.

Write Options That Are at Least 15% Out of the Money

The only options you should consider as writing candidates are those with no real (intrinsic) value, that are not in the money. Use only those options that are out of the money, which only have time (extrinsic) value.

Furthermore, you should select options that are significantly out of the money so that it will take a strong move in the stock—a move that normally would not occur in a two- or three-month time period (see secret #7)—to hit your bailout parameters.

These out-of-the-money options have a low probability of ever being exercised, or of ever having real value, and this low probability is a strong advantage to the naked options writer. In other words, choose to sell options that have the highest probability of expiring before the stock price ever gets close to the strike price.

Write Naked Options with No More Than Three Months Left in Their Life

Remember that as an option approaches expiration, its rate of depreciation normally increases, especially in the last month. Consequently, these are the times to write naked options.

You will receive a higher rate of premium in the last three months of the option than at any other time in its life. The shorter the time before expiration, the better.

Write Options That Are at Least 25% Overpriced

One of the most important secrets to successful naked option writing is to only write options that have beenoverpriced by the market, i.e., options for which the buyer is paying too much.

This will add insurance to your profit potential and is an important key to successful option writing. Make sure that the options you plan to write are at least 25% over the fair value.

Write Options Against Treasury Bills

When writing options, you must put up a margin requirement. The margin requirement can be in the form of cash or securities. It can be also be in the form of Treasury bills.

If it is the form of securities, you can only use the loan value of the securities. However, Treasury bills are treated just like cash, and this is one major advantage of using them.

Treasury bills will generate from 2% to 10% annually, depending on the money market, and this will be an added dividend to your option writing portfolio. Not only will you generate the profit from option writing, but you will also generate the return each year from your Treasury bills. Most brokerage houses place your credit balances in the money market, so you will still earn interest if you don't have Treasury bills.

Maintain a Strict Stock/Option Surveillance Program

Watch your stock and option prices like a hawk during the periods of time that you are holding these naked options positions. The professional naked options writer will keep a close eye on the price action of the underlying stock and will cover a position, bail out of a position, or buy back a position if there is a change in the trend of the underlying stock.

He will also take profits early when the option shrinks in value quickly because of an advantageous stock price move. Or he may take action when the options become extremely undervalued, according to the stock price. The closer you carry out a surveillance program, the better your profits will be, and the smaller your losses.

This surveillance program should also contain a continuous writing feature, which is best described as a method of reinvesting funds into new naked options writing positions as profits are taken. This process is similar to compounding interest in your bank account, except the return is much better!

By continually reinvesting in new positions and actively taking profits when they develop, your portfolio will grow at a much faster rate than is possible if you maintain a static program of waiting until the options expire.